|

|

||||

|

|

|

|

| |

|

|

| |

| 글로벌 트렌드 | 내서재담기 |

|

|  |

Reinvigorating the National Defense Industrial Base

As in the 20th century, the best way to ensure that a Cold War does not become a “hot one” is by one side maintaining an overwhelming lead in terms of both the quality and quantity of weaponry. Hitler invaded the USSR in 1941 because he realized that Germany enjoyed only a brief window of time before Soviet war production exceeded its own. That same year, Japan attacked Pearl Harbor realizing that delaying would permit the United States to dramatically upgrade its Pacific fleet and give it a permanent advantage in terms of offensive capability.

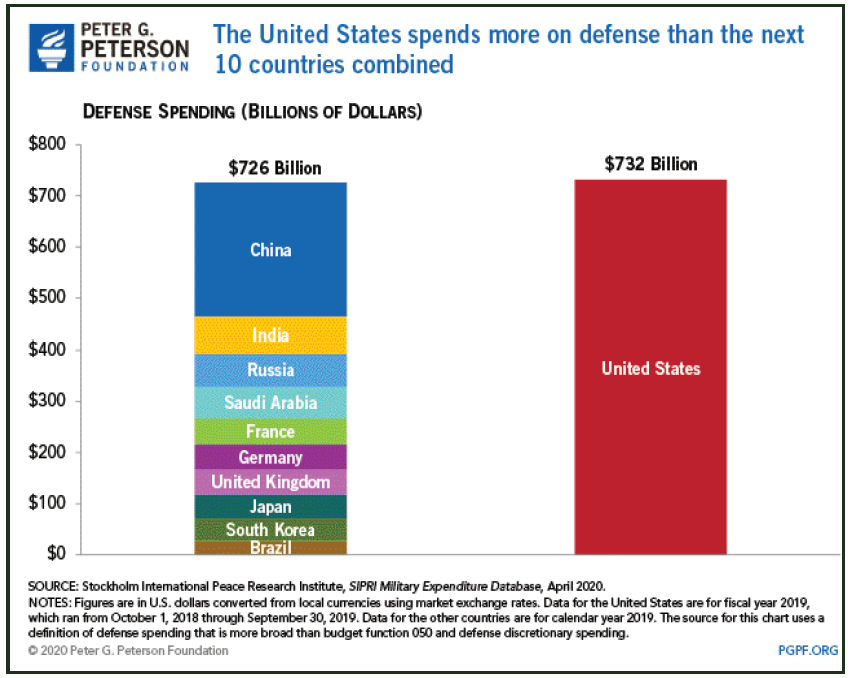

Today, the Chinese and Russians don’t hold an edge vis a vis the United States and its allies on any meaningful metric. From missiles to aircraft to warships to satellites to natural resources and logistical support, China, Russia and Iran can’t compete with the United States, Japan, and the UK.

As a result, military adventurism in Europe or Asia is preempted as long as America’s alliance makes sure the economic and military price to be paid for such aggression is prohibitive. And that’s only possible we can ensure that Russia and China never approach parity with the U.S.

Based on the 20th Century Cold War, the current portends a long war of economic attrition. This clearly favors the alliance with a larger and stronger network. And the biggest risks will likely arise from the kinds of “proxy wars” that trapped the United States in Vietnam and the USSR in Afghanistan.

Maintaining, the edge needed to win this war requires a highly competitive defense industry ready to respond to changing needs.

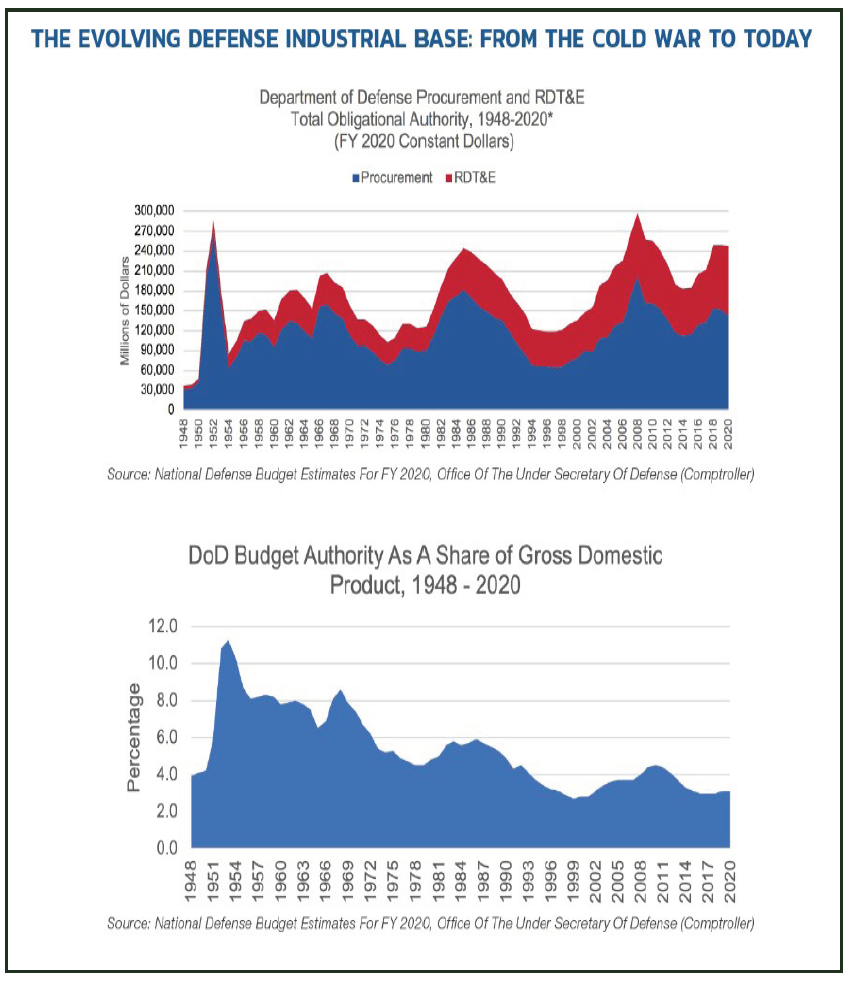

Since military procurement peaked during the Iraq war, America’s defense needs have changed dramatically. Following the terrorist attacks of September 11, 2001, U.S. forces concentrated on asymmetric warfare against dispersed non-state actors and their relatively unsophisticated state sponsors. To the extent that other superpowers were involved, it was in the roles of clandestine arms merchant or technical advisor.

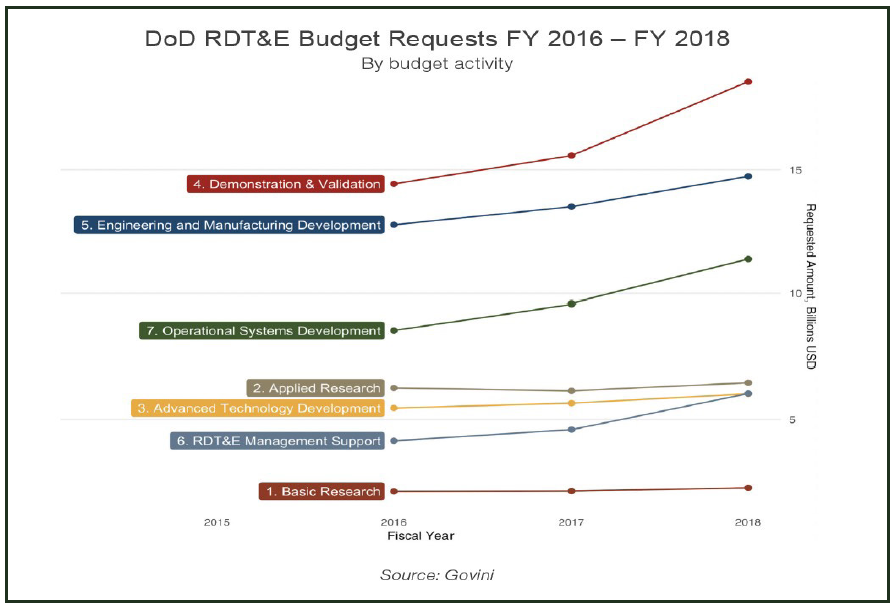

During the Obama years, Congress and the DOD recognized that the United States needed to stay on the cutting edge of military technology, but they were unwilling to commit to major procurement programs when the nature of future threats was so uncertain. As a result, procurement shrank, but R&D remained strong. So, while the military suffers from deployment shortfalls, it has a pipeline full of new state-of-the-art solutions ready to be rolled out.

Each year the National Defense Industrial Association (or NDIA) publishes a report card on the adequacy of America’s Defense Industrial Base to do the job of equipping the United States and its allies to meet anticipated challenges. This report card looks at 40 metrics grouped into eight categories: competition, production inputs, demand, innovation, industrial security, supply chain resilience, productive capacity, and political & regulatory constraints.

In a nutshell, America’s Defense Industrial Base has seen a surge in demand and production capacity as the Trump administration has worked to upgrade and replenish the arms stockpile while deploying new weapons, which were in developed during the Obama years. Meanwhile, it has seen a clear deterioration supply chain resilience, industrial security, and political & regulatory constraints.

Problems related to supply chain resilience particularly striking. These include being plagued by single sources of supply, fragile suppliers, foreign dependency, and other such risks. But fortunately, these problems are being aggressively addressed. As of January 2020, fourteen presidential determinations had been issued that focus on addressing strategic industrial base risks identified in a comprehensive DOD report. These determinations have indicated that materials such as sonobuoys, lithium seawater batteries, and critical chemicals for missiles and munitions needed special project funding to help mitigate the risks in those industries. By addressing these problems now, the defense industry will be more resilient when national security challenges arise.

Deterioration on the political and regulatory front is problematic, but not surprising. Defense preparedness is an area that gets a lot of attention from Congress when a new threat is “front and center,” but it’s easy to ignore when there are other more pressing concerns. Notably, as of last year, 77% of Americans polled by Gallup said that we were still “spending too little on defense.” As people realize that COVID19 and myriad other high-profile problems came from China and that China is working proactively (with Russia) to interfere with our political processes, Congress and the Administration will refocus on a multi-tiered defense strategy.

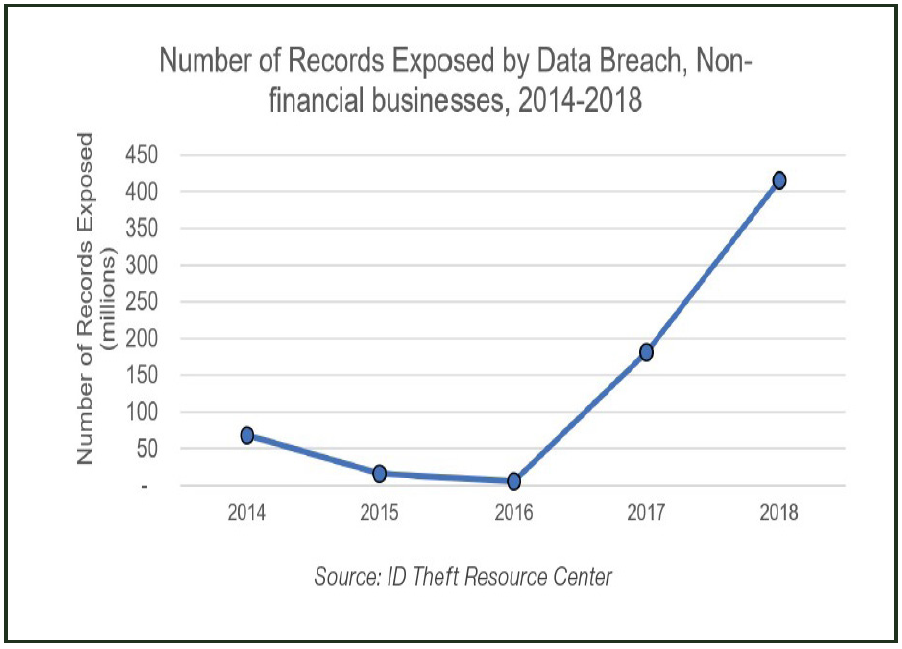

Meanwhile, by far the most alarming of the deteriorating categories are industrial security. In 2019, industrial security scored a 63, the lowest among the eight dimensions tracked. Furthermore, Industrial security has become increasingly relevant because massive data breaches by state and non-state actors have increasingly plagued defense contractors in recent years. According to MITRE Corp., new cyber vulnerabilities identified in the years 2016 to 2018 were almost double those discovered between 2014 and 2016. Given the high Russian and Chinese competence in cyber warfare, this is probably the biggest area of concern facing America’s defense industry.

Given this trend, we offer the following forecasts for your consideration.

First, the great battles of the 21st Century cold war will be fought in cyber-space with the support of human intelligence.

This is the one area in which China begins the war with a clear competitive advantage. However, it is probably the most volatile area of modern warfare, where competitive advantage can shift very quickly. Expect the United States and its allies to close the gap quickly as Chinese products and services are increasingly banned by OECD governments and firms.

Second, the recent deterioration in supply chain resiliency will be resolved as the DoD helps companies address single sources of supply, fragile suppliers, foreign dependency, and other such risks.

In the cost-driven, just-in-time era it is easy for companies to become overly dependent on supply chains that are not sufficiently robust. In normal times and in normal industries that’s often an acceptable risk, but when it comes to national security, it’s not. Until 2017, there was no formal mechanism for ensuring the resilience of defense contractor supply chains; but now there is. If all goes according to plan, we should almost never have a situation where a vendor fails to deliver because of upstream problems.

Third, America’s great strength is innovation and it will continue to lead in this area.

In an effort to translate the pipeline of innovations into deployed weapons systems the current administration has increased America’s already strong defense R&D budget. This advantage will increase as the United States and its allies work to erect “a technological iron curtain” shutting China out of the digital mainstream. Soon, consumers worldwide will be forced to choose between western products (including those from Japan and South Korea) and Chinese products. This is important because there are so many synergies between military and civilian technologies. During the 20th Century Cold War, the Soviets were severely handicapped by a lack of access to affluent Western consumer markets and the industries underpinning them. Until now, China has not had that problem, but sanctions related to everything from Hong Kong to religious minorities, to the intellectual property they will quickly take a toll on their ability to buy and sell mainstream technology. Over time, this will impede China’s ability to compete with western defense technologies, as well.

Fourth, by 2022 the DOD will succeed in reversing the recent deterioration in the National Defense Industrial Base caused by political & regulatory constraints. And,

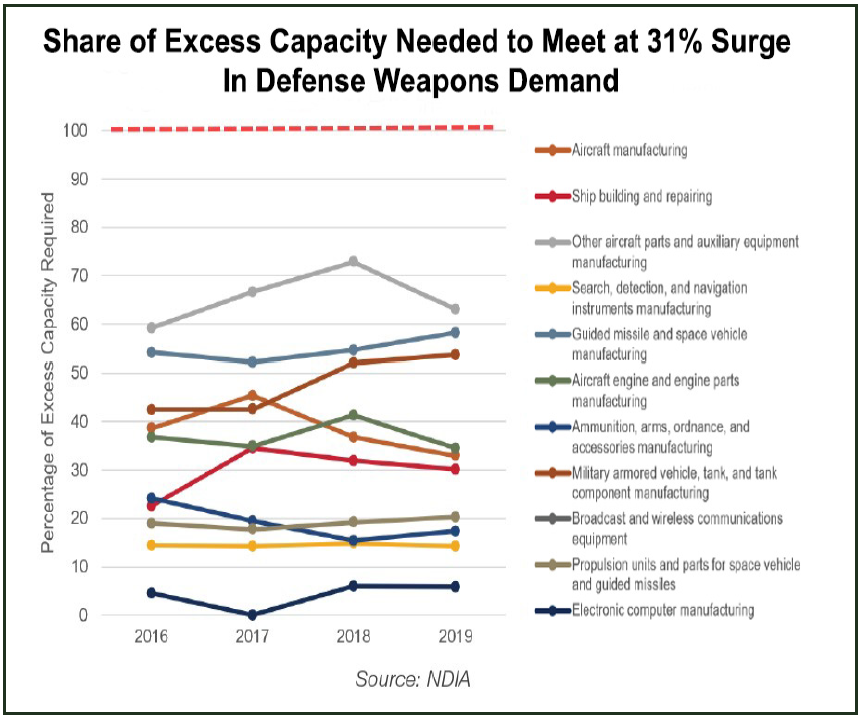

Fifth, America’s National Defense Industrial Base will be able to meet any demand surge we’re likely to face during the Sino-American Cold War.

Unlike a hot conventional battle, this will be a long, grinding “war of attrition.” Political and economic weapons are typically more important than arms in such a struggle. Arms and other resources are primarily useful for deterring aggression and “tamping down” hotspots. “Mega-programs like the renewal of America’s nuclear arsenal are undertaken over a decade or more, while a great deal of the resources goes into constantly upgrading existing platforms. Occasionally there are surges because of unexpected shortages, but the current administration has already minimized this contingency by making large one-time purchases of aircraft and missile components depleted over the prior decade. And in the event of a major conventional confrontation, the defense industry could readily accommodate a 300% surge in demand for consumables like ammunition and ordinance.

References

1. The National Defense Industrial Association. Wesley Hallman. Vital Signs 2020: The Health and Readiness of the Defense Industrial Base.

https://www.ndia.org/-/media/vital-signs/vital-signs_screen_v3.ashx?la=en

2. Washington Technology. February 5, 2020. Nick Wakeman. Is the defense industrial base in failing health?

https://washingtontechnology.com/blogs/editors-notebook/2020/02/ndia-defense-industrial-base-health.aspx

3. National Defense Magazine.January 31, 2020. Stew Magnuson. Special Report: Defense Industrial Base Vitality Outlook.

https://www.nationaldefensemagazine.org/-/media/sites/magazine/ebook/vitalsigns_ebook_final.ashx?la=en

.png)

.png)